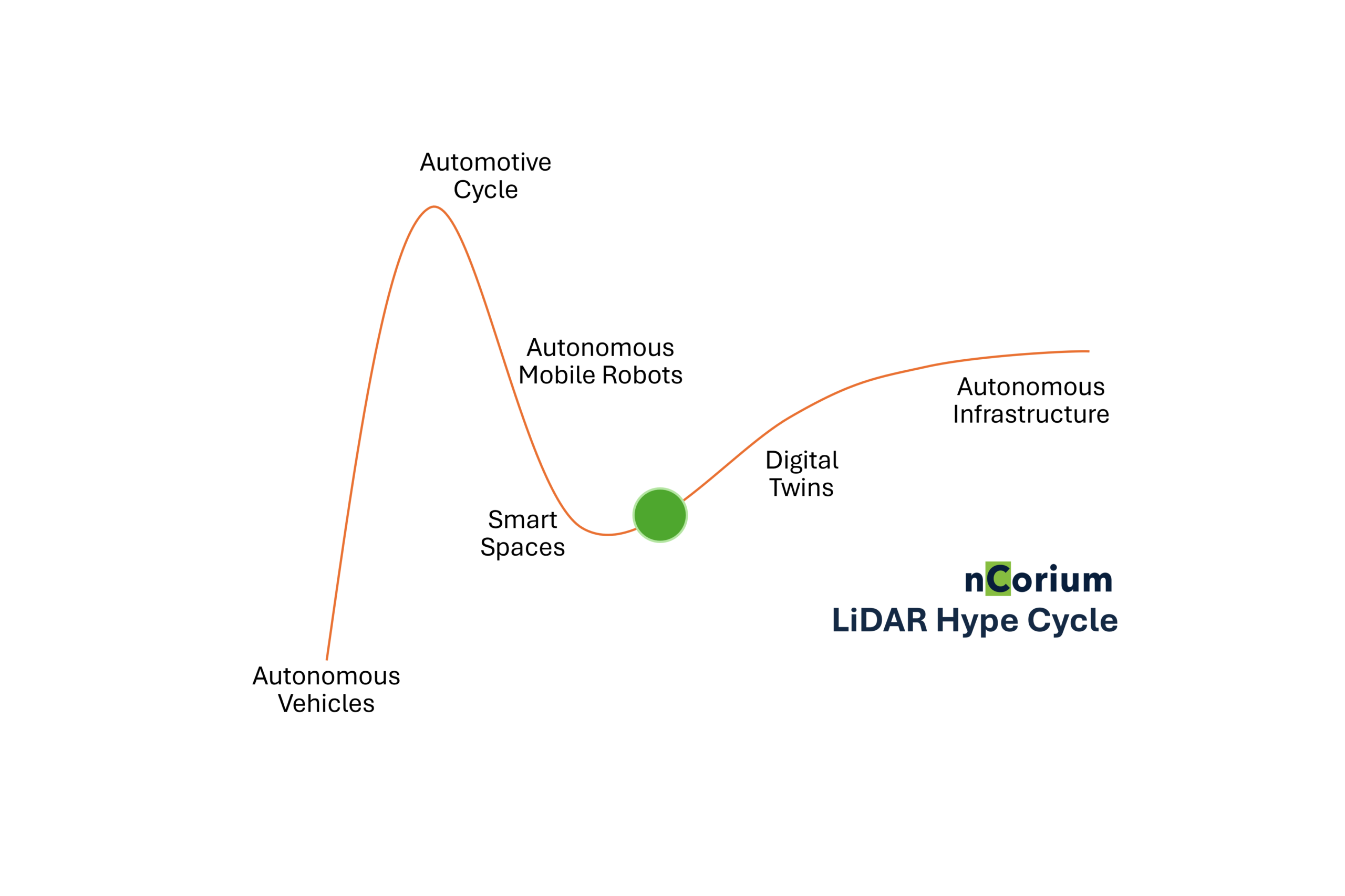

LiDARs are now entering the enlightenment phase of the LiDAR hype cycle with strong rebound in automotive and smart spaces maturing into digital twins for operations. Looking beyond automobiles, aviation, manufacturing, industrial, mining, rail, smart cities, and energy installations are set to undergo substantial transformation.

The LiDAR hype cycle traces the technology’s journey from anticipation of Autonomous Vehicles (AVs) to today’s maturing applications in smart spaces, digital twins, and autonomous infrastructure, with an eye on emerging opportunities.

Autonomous Vehicles (AV): The LiDAR Gold Rush

The period from 2010 to 2018 was the “Golden Era” of Autonomous Vehicle (AV) development, sparked by the DARPA Grand Challenges and Google’s early self-driving car tests. The catalyst arrived in 2010, when Google’s “Project Chauffeur” (now Waymo) began testing on public roads in California using Velodyne’s (now merged with Ouster) high-end HDL-64E LiDAR. This specific application created a “LiDAR gold rush.”

Market impact was immediate. By 2016, Ford and Baidu invested $150 million into LiDAR manufacturers, driving excitement about the technology’s rapid commercial evolution. Startups emerged with promises of solid-state units dropping costs dramatically. The prospect of shipping millions of LiDARs embedded in automobiles was exciting. Even if 1 out of 10 cars used LiDAR, that meant 1.5 million units every year from approximately 15 million cars shipped annually just in the United States.

Massive VC investments fueled hype, positioning LiDAR as the inevitable backbone of autonomous driving.

Western Automotive Cycle and Tesla Effect: Hard Brake on LiDARs

From 2019 to 2025, LiDAR adoption for AVs did not go as expected. Things turned sour pretty quickly. The retreat in the LiDAR hype cycle stemmed primarily from a mismatch between fast software development cycles and the automotive industry’s incremental feature rollout mindset and regulatory hurdles.

Then Elon Musk dropped the hammer in 2019, dismissing LiDAR as a “fool’s errand” in favor of a vision-only solution. Some investors questioned if LiDAR was really a necessity. Compounding this was the Western Automotive Cycle. Traditional OEMs in the US and Europe operate on 5-to-7-year product cycles. Validation barriers are steep: unlike a software update, a LiDAR sensor must be “automotive grade,” surviving 15 years of extreme heat, vibration, and road salt. While Chinese EV makers like Nio and Xpeng swap tech every 18 months like smartphones, Western giants like Ford and GM were hostage to legacy ecosystem. Ford and VW’s Argo AI shutdown in 2022 signaling a retreat from LiDAR based ADAS toward simpler, camera-based ADAS.

Partial ADAS and Autonomous Mobile Robots (AMRs): Holding the Fort

As the AV hype deflated, expectations in the automotive industry tapered from full autonomy to partial ADAS, allowing breathing room for safe, incremental evolution. Auto providers continued to invest, with more than 50% of LiDAR shipments still driven by the sector, including fleets and personal vehicles. As of early February 2026, Waymo itself has logged nearly 200 million fully autonomous miles on public roads.

In parallel, Autonomous Mobile Robots (AMRs) in warehouses quietly played their role. AMRs adopted the technology around the same time as AVs, but at a smaller scale and with less public awareness. Early 2D LiDAR scanners (like those from Hokuyo) became common in research and industrial AMRs in the late 2000s, used for simpler obstacle avoidance rather than the complex 3D mapping needed for high-speed road travel.

The key contribution of AMRs is revolutionizing operations and enabling true automation, delivering efficiency gains in e-commerce and supply chains. This created a scalable template for operations beyond warehouses. AMRs’ success now serves as the foundational proof-of-concept for the big prize: autonomous infrastructure, where LiDAR acts as the reliable “eyes” enabling self-regulating cities, factories, and ecosystems.

Consolidation and Smart Spaces: The Inflection Point

At the lowest point in the LiDAR hype cycle, the LiDAR industry consolidated, marking an inflection point toward maturity. Early moves included Ouster’s merger with Velodyne (2022) and Cepton’s acquisition by Koito (announced 2024). Partnerships expanded, like Innoviz with BMW for solid-state sensors.

Recent 2025-2026 activity accelerated this: MicroVision acquired Luminar’s Iris and Halo assets for $33 million, gaining IP, talent, and contracts; Ouster bought vision firm StereoLabs for $35 million plus shares (2026) to fuse LiDAR with AI perception for robotics and industrial uses.

The pivot to smart spaces (buildings, campuses, security) provided a breather, reviving potential through broader applications and large shipment volumes. Quanergy refocused here, while Innoviz advanced mass-market expansions.

Market signals are positive, with global LiDAR at ~$2.9 billion in 2025 growing to ~$3.3-3.5 billion in 2026, driven by non-AV diversification.

Automotive Rebound and Digital Twins: The Enlightenment Phase

Driven by strong trends in automotive and with smart spaces maturing into digital twins for operations, LiDARs are now entering the enlightenment phase of the LiDAR hype cycle. Looking beyond automobiles, aviation, manufacturing, industrial, mining, rail, smart cities, and energy installations are set to undergo substantial transformation.

The aviation industry is leading the pack. Having invested significant resources in exploring LiDAR hardware over the years with PoCs and Pilots, many leading airports in US, Europe and Asia are moving to implement digital twins and applications that help everyday operations.

The 2026-2028 period is going to see the unveiling of groundbreaking solutions that are generationally different from what we have been used to for decades. In airports, most of the visible improvements in recent times were focused on aesthetics, through architecture and design of airports. With operations platforms built on LiDAR networks, we will now see substantial upgrades to passenger operations and passenger experience.

Digital twins offer considerable potential by enabling real-time monitoring, predictive analytics, passenger flow management, asset management, safety, compliance, and most importantly passenger experience. In the hype phase, the AV focus limited scope, but eventual consolidation and discovery of smart spaces broadened it to practical, scalable use.

There are initial indicators that other verticals are watching this space, and it is our assessment that they will soon start investing resources into PoCs and pilots just as airports did since 2020.

Autonomous Vehicles to Autonomous Infrastructure: The Big Prize

Imagine cities operating by themselves, sensing the surrounding environment, managing people, vehicles, and traffic flows, and achieving order. Picture factory automation at scale.

We don’t need to go far. The AMRs in warehouses are already showing us what is possible. With reliable navigation and coordination, LiDAR plays a significant role in high-impact settings. This foundation extends to broader ecosystems: smart grids optimizing flows, urban sensing for seamless safety and efficiency, and self-regulating industrial operations.

The early gold rush narrowed vision to AVs, deflation forced diversification, and consolidation built resilience. Integration challenges abound, but with grounded execution and cross-functional collaboration within these verticals, while balancing cost and reliability, we are looking at explosive growth of LiDAR sensor-based infrastructure.

Beyond LiDAR Hype Cycle : Real World Impact

We at nCorium are passionate about ideas that advance practical progress and are genuinely excited about these developments. Our analytics platform, domain-specific workflows, and applications form the essential bridge between sensors and end-user experience in airports and beyond.

As the LiDAR landscape matures into practical applications across smart spaces, digital twins, and autonomous infrastructure, expertise in sensor fusion and operational intelligence becomes increasingly valuable for turning raw data into reliable, actionable outcomes. If you want to know more or collaborate, reach out at info@ncorium.com or reach us through Contact Us